Secrets from a Top Portfolio Manager

How ASA became the best-performing precious metals fund over the past seven years

Since the current investment process was implemented seven years ago, ASA has generated cumulative returns of more than 500%. More remarkable still, ASA has outperformed all peers on both an absolute and risk-adjusted basis.

So what’s the secret sauce?

Those who have followed me for some time know that I rarely focus on performance alone. Throughout my career, I have cared far more about the investment process and macro context. Over time, performance follows.

Some History

ASA (or the “Fund”) was founded in 1958 to provide U.S. investors access to South African precious metals mining companies, at a time when direct investment in these companies for US investors was not possible.

ASA was a standout performer during the financial crisis, reaching over $900 million in net assets in October 2008. Three successive tender offers and a protracted bear market later then drove, assets to a low of $190 million in 2018, by which point ASA had become a sleepy, somewhat index-hugging portfolio with only a 3% portfolio turnover.

The Fund was internally managed, and the Board sought to appoint an external manager, in part to move from a high fixed cost internal management model to a more industry standard external adviser compensated on a percentage of assets managed.

In April 2019, shareholders of ASA appointed Merk Investments LLC (“Merk”) to manage the fund and Peter Maletis – who had spent a decade at Franklin Templeton’s gold fund – was appointed as portfolio manager.1

Assets at the time were approximately $230 million. Peter repositioned the portfolio quickly, and performance accelerated in the early period. Later, the Fund faced headwinds during the “higher for longer” environment which compressed some valuations, especially those of the more junior mining companies.

In 2022, Jamie Holman, previously the number two at Invesco’s precious metals fund, joined Merk and helped position the Fund for what was to come.

As of this writing, ASA has grown - net of dividends, share repurchases and expenses - to $1.5 billion as of May 15, 2026.

The Secret Sauce

ASA employs a bottom-up fundamental analysis and relies on detailed primary research including meetings with company executives, site visits to key operating assets, and proprietary financial analysis in making its investment decisions. Risk is managed through regional diversification at the asset level and a deep understanding of geopolitical risks. ASA employs a long only concentrated strategy with low turnover.

The scarcest resource in precious metals mining is good management. While other factors matter, developing and operating a mine successfully depends on management that understands not only the geology and operations, but also the needs of all stakeholders. Merk believes management that works constructively with all stakeholders is more likely to succeed.

How does Merk identify good management? We often describe Merk’s investment approach as “venture capital light”. In practice, this means backing proven teams – those with a track record are more likely to secure funding than unproven teams, even those with geologically promising resources.

Even larger mining companies are steadily depleting a finite resource. While a return of capital through dividends is welcome in the current environment when margins are high, we want the money to be re-invested into additional exploration, adjacent land, or selective acquisitions – particularly when led by management teams we trust.

Notably, we also look for catalysts beyond a potential appreciation in the price of precious metals. This is why Merk often invests early in exploration or - these days - development companies. Much like venture-funded tech businesses, these companies get funding for only a year or two before they return for more capital. To the extent they meet their targets, larger investors are joining in future funding rounds at often significantly higher valuations. We have helped “institutionalize” numerous mining companies - our largest holdings were small development companies just a few years ago.

Good management teams attract investors. Understanding a company’s investor base is therefore critical, particularly in assessing whether capital will remain available in the next funding round.

ASA’s closed-end structure provides relatively patient capital, without daily inflows or outflows. At the same time, it requires active capital allocation - recycling capital from existing positions into new opportunities, while balancing conviction and diversification.

Different from high tech VC investing, when a company does not succeed, the gold in the ground is still there, meaning a new operator might be able to jump start a project.

Unlike ETFs, we can participate in funding rounds, often with warrants attached.2 Warrants are helpful tool for a company as it provides a path for future funding; and they are great for investors that receive the right to provide further funding at set price.

Ultimately, the “secret sauce” is our investment process.

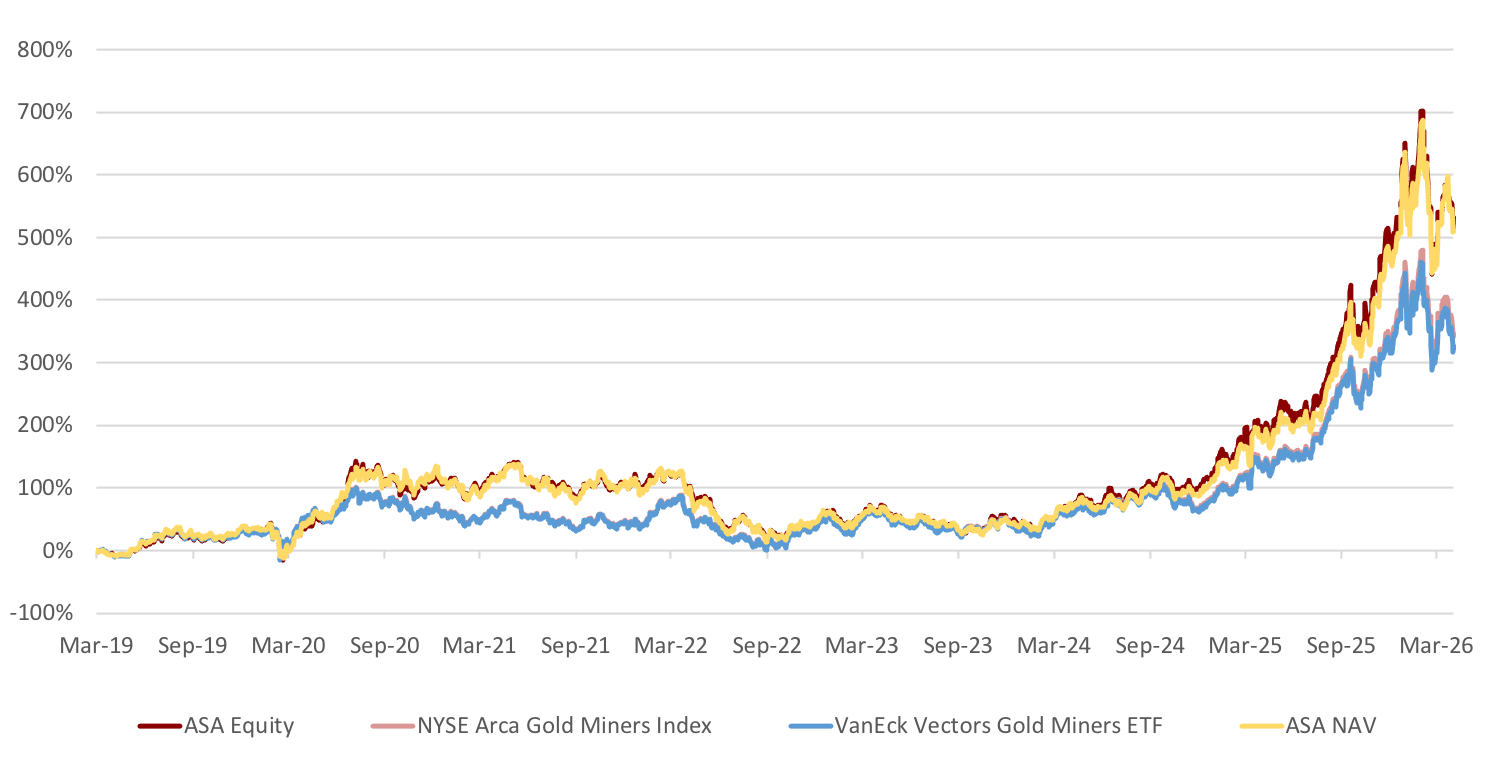

The Performance

Below is ASA’s performance relative to indices since April, 2019, when Peter Maletis started managing the Fund.

You will see a reference to the performance of the net asset value (NAV), as well as that of the share prices (Equity).

Data as of April 30, 2026. Source: Bloomberg

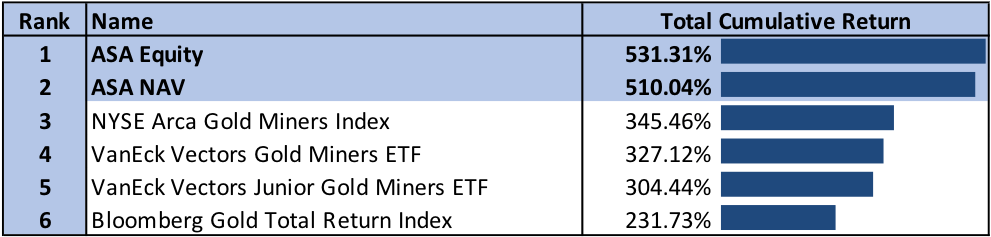

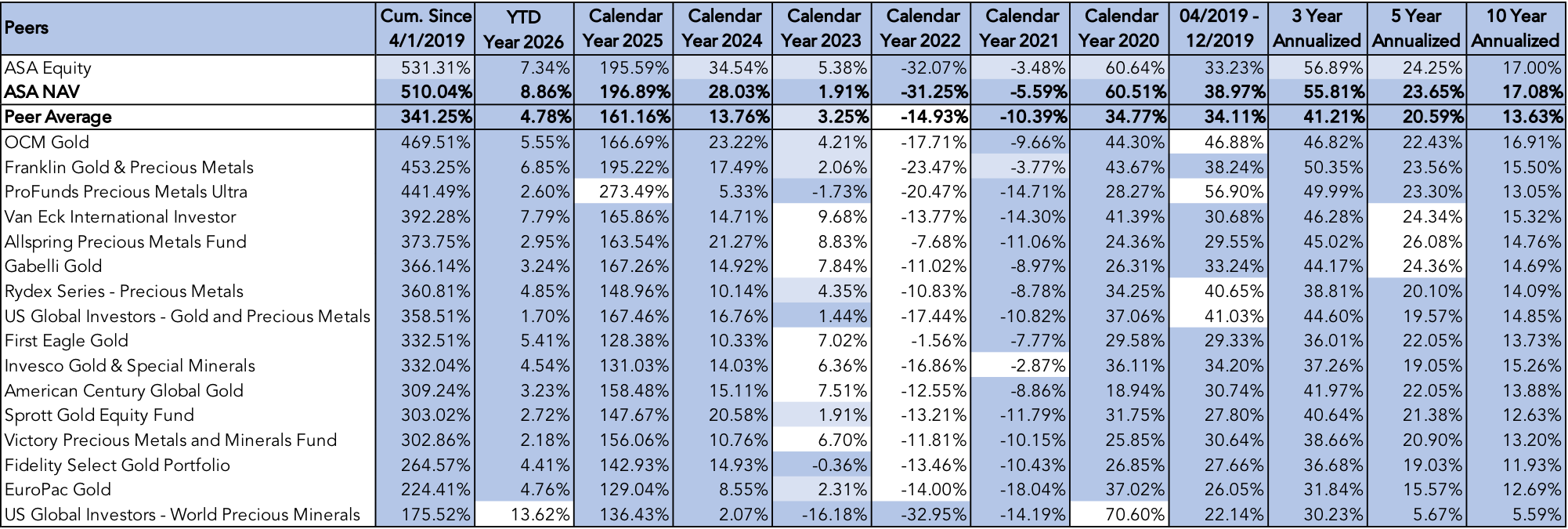

Peer performance over various periods:3

ASA’s ranking over various periods:

ASA’s Equity returns are included in the rankings above. For example, since April 1, 2019, ASA’s NAV ranks #2, with only ASA’s Equity ranking higher. ASA’s Equity outperformance relative to NAV reflects shareholder gains from both portfolio performance and the narrowing of ASA’s share price discount to the NAV during much of Merk’s tenure.

If you divide the returns by the risk (volatility), the Fund continues to come out on top over the seven years that Merk has managed ASA.

Outlook

In 2011, Marc Andreessen published his famous essay “Why Software is Eating the World.” Software provided the promise of low barrier to entry, high margin products. Why would you invest in mining when you can invest in software? The bull market in precious metals was just turning into what would become a protracted bear market at the time.

Fast forward to today, and “AI is eating software.” A current hallmark of AI, however, is that barriers to entry are high (massive investments are required) and margins uncertain. For the first time in a long time, there is a level playing field between technology, industrial and mining investments. Precious metals mining also has high barriers to entry and the potential for high margins. This shift is reflected in growing interest from generalist portfolio managers, particularly in mid-sized mining companies. Given the relatively small size of the sector, increased participation can drive meaningful valuation re‑rating.

This is not the time and place to make a prediction about the price of gold, and this is not investment advice - the precious metals mining space is a highly volatile space and not for everyone. But given that interest in the space has been broadening, our track record demonstrates that traditional bottom-up active management can succeed.

I’m incredibly proud of my team that has enabled this successful investment approach. An independent analysis by Broadridge concluded that ASA’s outperformance has been driven not by excessive risk-taking, but rather by the discipline of the investment approach itself.

ASA recently announced the extension of Merk’s advisory agreement for 90 days through June 30, 2026.

Follow me at x.com/AxelMerk, and feel free to reach out with questions.

Axel Merk

President & CIO, Merk Investments

Certain Tax Information: ASA is a “passive foreign investment company” for United States federal income tax purposes. As a result, United States shareholders holding shares in taxable accounts are encouraged to consult their tax advisors regarding the tax consequences of their investment in the Company’s common shares.

This report was prepared by Merk Investments LLC (“Merk Investments”),and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments makes no representation regarding the advisability of investing in the products herein. The information contained herein reflects Merk Investments’ current views and opinions with respect to, among other things, future events and financial performance. Charts, graphs, and tables are provided for illustrative purposes only. Any forward-looking statements contained herein are based on current estimates and expectations. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice and is not intended as an endorsement of any specific investment. The information contained herein is general in nature and is provided solely for educational and informational purposes. The information provided does not constitute legal, financial or tax advice. You should obtain advice specific to your circumstances from your own legal, financial and tax advisors. Past performance is no guarantee of future results.

Peter Maletis started managing ASA on April 1, 2019. On April 12, 2019, ASA shareholders approved Merk Investments as ASA’s investment manager. On April 1, 2022, Jamie Holman joined the ASA portfolio management team at Merk Investments.

The regulations don’t prohibit ETFs from participating in funding rounds, but given that ETFs have a daily arbitrage mechanism to have the underlying NAV mirror the share price, market makers don’t like anything they can’t hedge or model. In our analysis, the precious metals mining sector is already the one with the greatest dispersion of returns (active management matters!); when you start participating in funding deals, we understand the larger market makers have little appetite, de facto creating an environment were ETFs don’t participate in a good portion of the market where ASA is active in.

The ten-year performance includes three years from the previous portfolio management team.